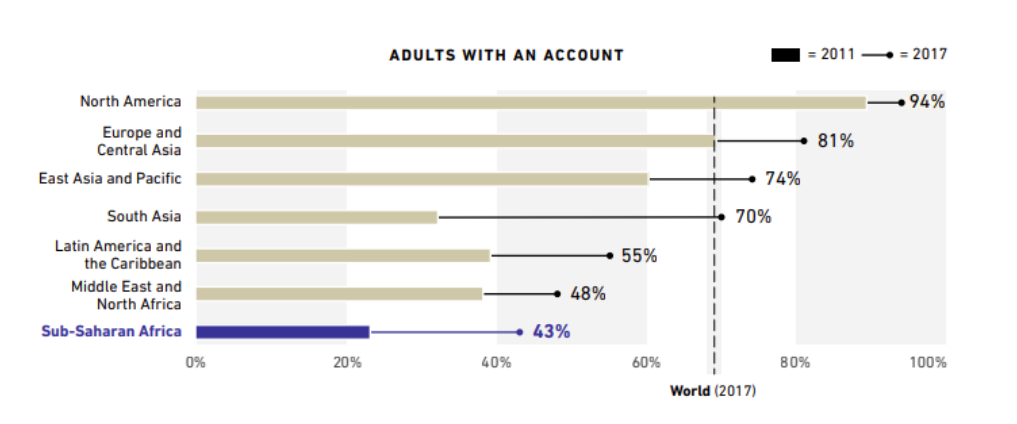

Back in 2017 the problem of living without a bank account (read: financially excluded) accounted for millions of people with huge gender gaps. And though the situation has been improving over the years, Africa is still far away from the world average.

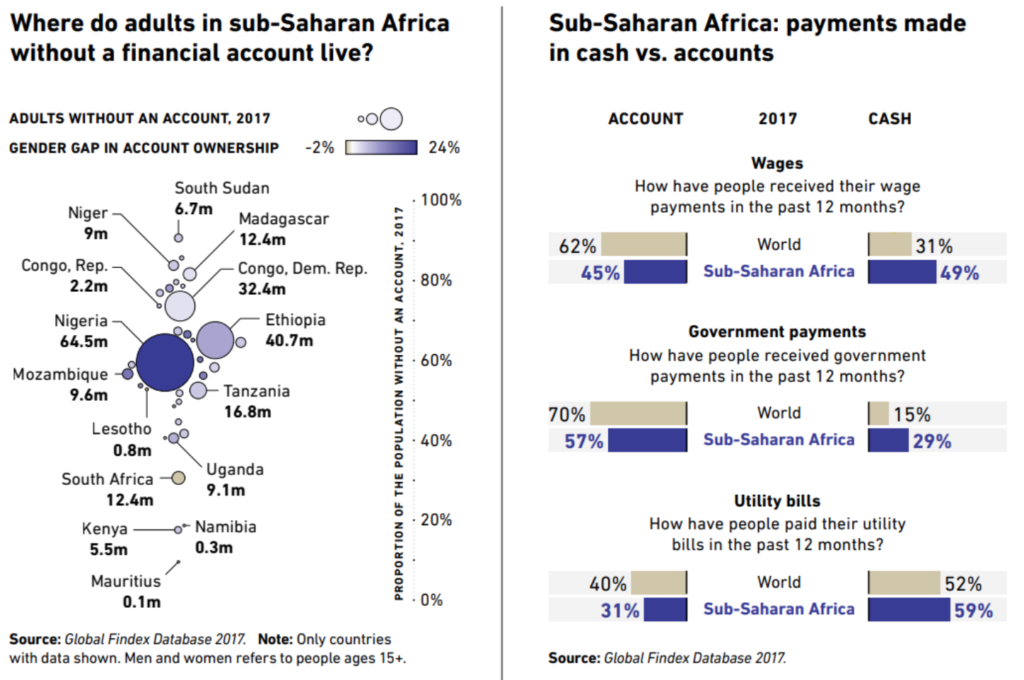

Also, scale of the problem varies: while countries such as Kenya managed to keep the proportion of their financially excluded population around 20%, other regions similar in size (South Sudan) suffer a dramatically worse (90%) exclusion rate.

Yet, the situation can and should be changed.

Financial goods and services have to be made available and affordable to all local and global entrepreneurs, regardless of their specific net worth or scale. But first, achieving financial inclusion means eliminating barriers that prevent people from engaging in and utilizing the finance market to better their lives.

What are those barriers?